2025 EM Outlook: Reading the tea leaves

Finding Alpha in an emerging multipolar world

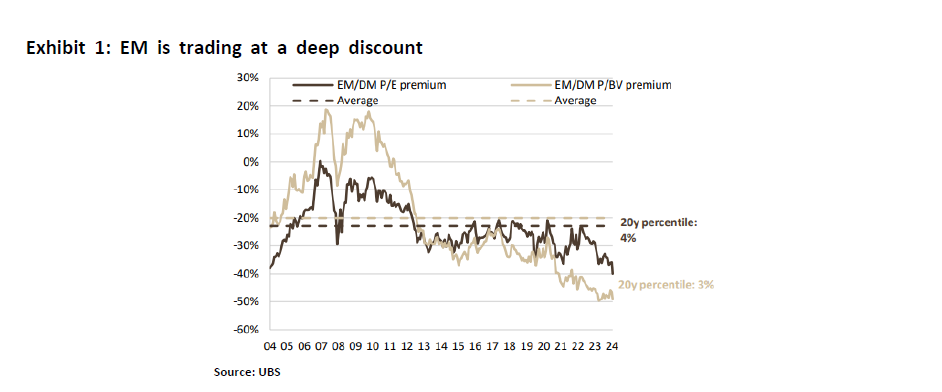

We are at an inflection point for emerging market equities. In 2024, the MSCI EM index returned 18.5% (AUD) and we expect positive momentum to continue through 2025 given robust fundamentals in EM economies.

Emerging markets equity have derated and despite very attractive valuations, investors remain underweight the asset class. In our view, the recent period of underperformance is an outlier as the outperformance of developed markets was boosted by aggressive fiscal spending and accommodative Central Banks.

The fundamental investment backdrop is shifting. Developed economies are beset with growing public deficits. Prolong elevated inflation is causing many Central Banks to remain vigilant. In contrast, in many emerging markets, fiscal balances are healthy while debt to GDP ratios are at reasonable levels. Corporates are in healthy positions.

In 2025, we are likely to see weakening of the US Dollar as momentum peaks and structural concerns re-emerge. The persistent large US federal government debt and the uncertainties in implementation of new government policies may impact economic growth and are likely to temper expectations of continue USD strength. Emerging markets returns are likely to improve.

We remain optimistic companies and outlooks in 2025.

• Many developing economies have endogenous growth drivers. Governments have undertaken decades of economic reform. Infrastructure and manufacturing capabilities are much improved than years past. Their growing middle class aspire to a higher standard of living. These young countries will be able to grow at a fast clip in a generally slow global economy.

• Attractive stock market valuation. Many stocks offer attractive dividend yields and earnings growth. Further funds flow can drive their valuations.

• Finally, there are ample opportunities in China. The perceived structural problems in China are well known and discounted by the cheap valuations of Chinese stocks. Recent policy changes have led to price increases in major cities, monetary policy has shifted from prudence to “moderately loose”, and fiscal policy is expected to relax further.

Market Commentary: Volatility creates opportunity.

We believe the short-term focus on protectionism and trade tensions provides an opportunity to buy quality franchises across EMs as many emerging economies are poised to grow solidly in the coming years relative to developed markets.

Ox Capital is currently over-weight China, Indonesia, and Vietnam and underweight India, Taiwan, and Korea. We are predominantly focused on the bright spots in emerging markets where the environment is ripe for outperformance.

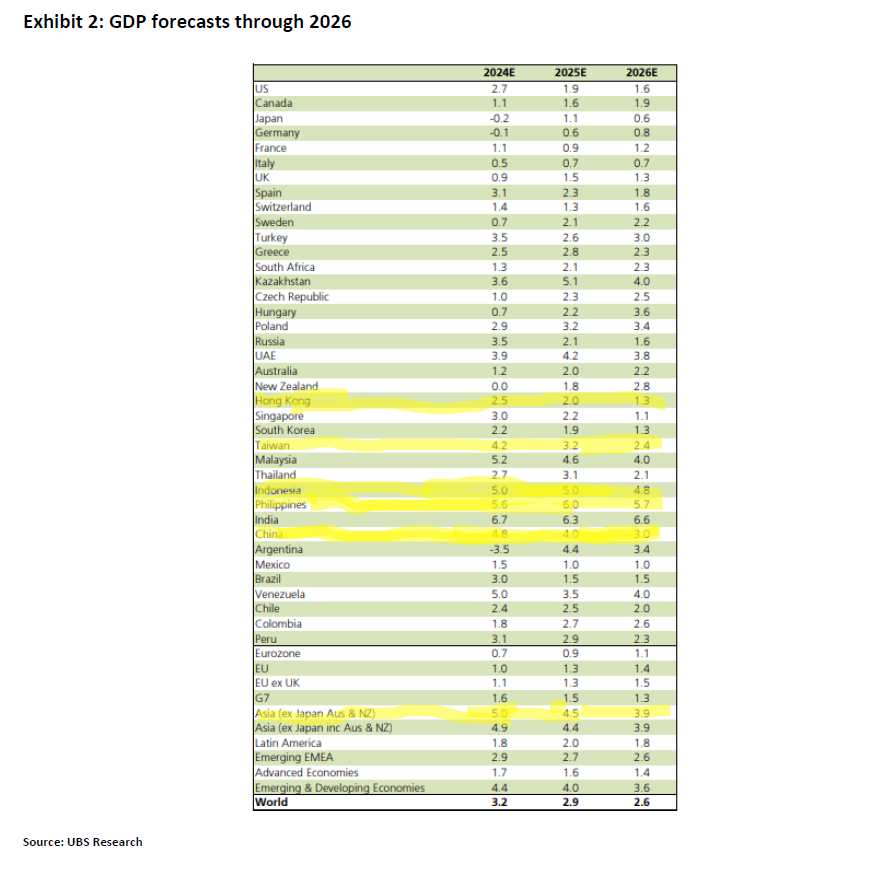

China: Looking through the noise. The issues facing the Chinese economy are well understood and manageable. Despite geopolitical tension and correction in the property sector, the Chinese economy grew solidly (≈5%) in 2024. Noticeably, it has been over three years into the downturn and new property sales volumes have already adjusted sharply from peak. At the same time, secondary property sales remained resilient, indicating fundamental demand for better living quality in China. In our view, the domestic economy is gradually bottoming and the property market will pick up as confidence returns. In 2025, the Central government is committed to deliver solid economy growth.

We expect geopolitical competition to persist in 2025. The new US government will likely impose trade tariffs on its trading partners. While no definitive polices have been announced, some economic forecasts indicate that a unilateral 60% tariff (which we believe is unlikely to be applied in full) on exports to USA will hit China GDP by ~2%. We believe this potential “headwind” to growth is manageable. We note:

• The Chinese government will support the economy as needed, to deliver on its growth target of 4.5%-5% in 2025. China will actively use fiscal and monetary measures to counteract economic impacts of tariffs. We believe the recent China policy pivot is highly significant, with measures to support focused on stabilizing the housing market, fight deflation, and reflate the

economy.

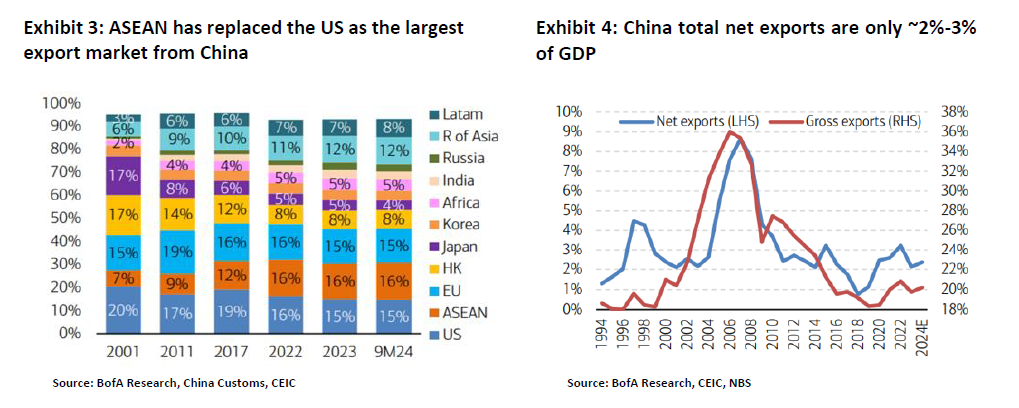

• China has developed other export markets. While USA remains an important trade partner to China, its importance has been declining. In 2017, USA accounted for 19% of China’s exports, but it has dropped to ~15% in 2024. In contrast, ASEAN now represents ~16% of exports, up from 9% in 2011. Moreover, exports is not as big a part of the Chinese economy as most believe, it is only about 20%. So direct export to the US is only around 3% (20% export x 15%) of China’s GDP.

• Diversification of supply chains: Furthermore, companies in China have relocated supply chains that are more labour intensive in other regions to mitigate impacts from tariffs and to take advantage of the cheaper labour costs. In many cases, the key components may still be produced in China, with the assembly done outside. Over the last decade, Chinese companies’ technological advancements have lifted the quality of the exports mix. China has become the centre of global supply chain of many key components and high value products. It is going to be highly costly to shift away from China’s supply chain.

Despite the firm stance the U.S. has maintained toward China over the past eight years, recent statements from the incoming Trump administration suggests a reassessment of the relationship between the two nations is probable. We are hopeful of stabilisation of relationship between the two countries, driven by mutual interests.

Finally, the funds flow problem facing the HK equity market is likely to be at least partially ameliorated by the continuation of the inflow via the China Connect program. In 2024, greater than USD100 billion dollars have flowed into the Hong Kong market, adding to the sustained inflow since the start of the program in 2013. To the extent that outflow in the Hong Kong is a drag to valuation, the rising Mainlander and local ownership offset that somewhat.

We remain focussed on companies that are going to be longer term champions domestically and globally. Vast majority of our positions are not exposed to trade tension between USA and China. We own domestic champions who are winning market share and growth will accelerate as the domestic economy reflate. Moreover, many companies in the portfolio are developing global franchises such as BYD, CATL, Trip.com. These companies are building strong relationships with countries around the world and gaining market share without exposure or relying on the US market for growth.

Taiwan & South Korea: Positioned to benefit from the continued AI (R)evolution.

A significant portion of the global technology supply chain is concentrated in Taiwan and South Korea. The rapid push by major companies and hyperscalers worldwide to implement AI strategies has created an unexpectedly strong demand for semiconductor chips. This surge provided substantial benefits to South Korean and Taiwanese suppliers.

The outlook for 2025 remains positive, buoyed by the region’s strong position as a global leader in semiconductor manufacturing (TSMC) and advanced technology innovation, such as High Bandwidth Memory (SK Hynix). Put it another way, the AI revolution cannot advance without the likes of TSMC and SK Hynix.

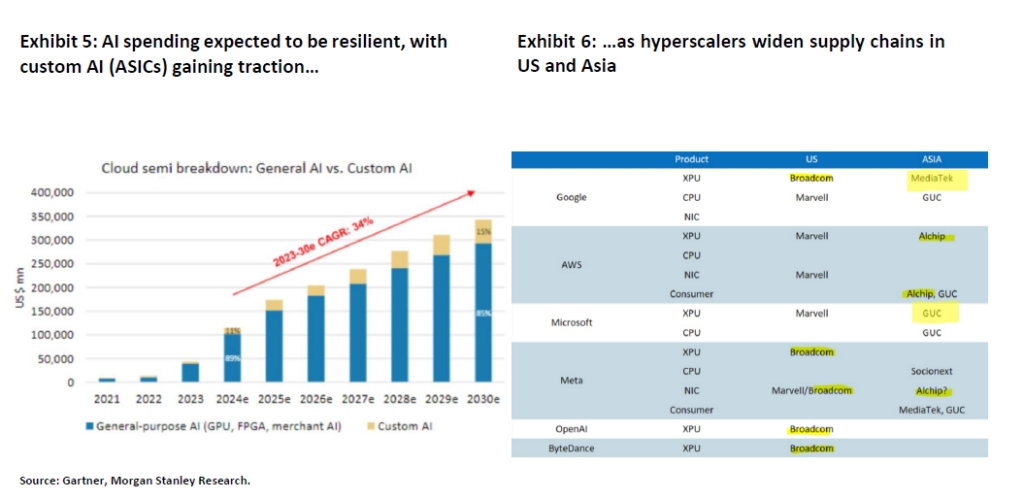

• We anticipate that the AI technology spending is likely to continue, with ASICs (Custom AI chips) spending becoming more prominent in 2025.

• In our portfolio, we own TSMC, the dominant global leader in semiconductor foundry services. For example, TSMC is winning >95% of AI projects. Furthermore, AI datacentre contribution is growing strongly, from 6% of revenues in 2023 to over 30% by 2027. As AI demand continues to broaden, TSMC is set to benefit and grow earnings strongly.

ASEAN: A vital region to the world.

The economic outlook for 2025 remains robust for the ASEAN region, supported by strong domestic consumption, growing intra-regional trade, and foreign direct investments. Regional integration under the ASEAN Economic Community (AEC) is expected to further strengthen the block.

Indonesia: An economic powerhouse. The Indonesian economy is undergoing a dramatic economic transformation that is underpinned by a young and growing population, abundant natural resources, and its strategic location in the Asean region. Companies such as BYD, are building plants in Indonesia to manufacture EVs for the domestic and export markets. Indonesia has also seen increasing investment in AI infrastructure, as global hyperscalers (Microsoft, Amazon, etc) are increasing their presence in country. We believe the environment & outlook is supportive of equity market performance, which are currently on cheap valuations relative to history.

• A robust economy. Real GDP is expected to grow at ~5% through 2025 per the IMF. The government is fiscally responsible (deficit of ~ 2.5% of GDP). Its external trade position is healthy thanks to resilient commodity demand and improving manufacturing capabilities.

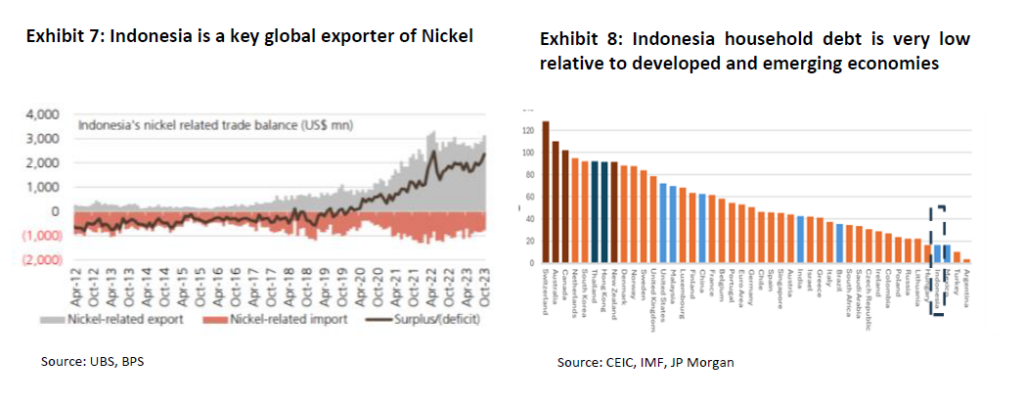

• Low indebtedness. Indonesia households are less indebted compared to many other economies, at just ~10% of GDP. For example, Australia household debt is much higher at ~116% of GDP.

• Demographic Dividends. Indonesia is the world’s fourth-most populous country, with ~280mn people, representing a huge domestic market. The median age is around 30 years old, a young demographic that supports both consumption and employment growth which will sustain economic expansion longer term.

• Abundant natural resources. Indonesia is rich in natural resources & commodities, such as oil, gas, coal, palm oil, and minerals like nickel. These resources provide a steady stream of export revenue and attract foreign investment. In fact,

Indonesia is the largest producer of nickel in the world, producing over half of global supply. We expect this will benefit Indonesia’s terms of trade, and fuel investment growth for years to come.

There has already been infrastructure spending in this domain including large plant installations to convert the countries surface layer Nickel to be processed into battery grade nickel. Electric vehicles and batteries makers are set to invest in Indonesia to bolster their nickel supply chain.

• Strategic location for trade & nearshoring. Foreign direct investment (FDI) continues to stream in, seeking to provide more quality goods to increasingly wealthy Indonesians and to use Indonesia as a manufacturing base to export to Western markets. This trend is underpinned by improving infrastructure and abundance of skilled labour.

Vietnam: The next manufacturing hub to the world. Vietnam is riding the wave of current global supply chain reconfiguration, boosting its GDP growth. Greater foreign direct investment into an ever more open and market driven economy. Unemployment rate is consistently low in the country (≈2.25%). The rising middle class is in turn demanding higher quality goods and services, in an increasingly urban setting. With a population of just under 100M people, and a urbanisation rate of under 40%, Vietnam reminds us of China ~15-20 years ago. There is substantial room for growth in the coming years. As such, we believe this backdrop provides a foundation for alpha generating opportunities.

• Solid FDI growth: Vietnam has been successful in attracting foreign direct investment (FDI) into the country. Commitments have been seen across thousands of projects and recent strong FDI inflow will support Vietnam’s ability to continue this journey of industrialisation, boosting exports, supporting domestic investments, whilst also creating new jobs.

• Manufacturing powerhouse to the world. Vietnam’s ability to continue to attract significant FDI flows, even amidst the current global environment, is proof of the increasing competitiveness of Vietnam’s manufacturing sector amongst global supply chains.

• Increasing production demand. We have seen announcements from companies such as Apple, and its supply chain such as Foxconn, Luxshare and Goertek, moving manufacturing to Vietnam with increasing frequency. Key production of AirPod and more complex products such as Apple Watch and iPad are planned to be increasingly offshored to Vietnam over the next 3 years.

• Extensive Trade Agreements in place already. Vietnam’s obvious locational benefit, in close geographic proximity to China, continues to be enhanced by greater regional and country-based partnerships and free trade agreements (FTA). Vietnam has more free trade agreements in place than any other countries globally.

LATAM: Near term volatility, but long-term opportunity

LATAM represents roughly 1% of the world index and ~9% of the EM index. Ox Capital is underweight Brazil and Mexico in LATAM given near term headwinds in each market (which we explain further below).

The LATAM index is dominated by financials, followed by materials, consumer staples and energy & commodities. As the global economy expands, and energy transition accelerates, supply and demand for critical minerals will tighten, resulting in positive implications for the LATAM region. Long term, we believe exposure to the region is crucial for investors given:

• Strong FDI inflows. LATAM remains a prospective destination for foreign direct investment (FDI), given LATAM is a resource-rich region with a rising middle class and is short on world class infrastructure.

• Key global minerals suppler. The LATAM region has an abundance of natural resources. Commodity exports make up 60-90% of the region’s external trade. LATAM is a key producer of critical minerals to the world, including Silver (50%), Copper (40%), Lithium (35%), and Zinc (>20%). Importance of these metals will only grow as these minerals among other rare earth metals are essential to the alternative energy transition. As developing countries, particularly in Asia, continue to grow, demand for resources will continue to intensify. LATAM will be a key supplier and beneficiary.

• Nearshoring and reconfiguration of global supply chain. Nearshoring is a significant opportunity for the LATAM region in the coming years based on their geographical proximity to North America, and relatively cheap and skilled labour.

Mexico’s relationship with the US is already well-established, as it is the largest exporter to the US. The country’s ~15% share of US imports has now surpassed China’s ~14% and China’s share of imports has been in decline since its peak in 2017 with further declines post the implementation of the United States – Mexico – Canada free trade agreement (USMCA). Moreover, Mexico’s domestic logistic infrastructure is well developed with over 100 airports with direct flights to-and-from the US and Canada, industrial zones that are connected by over 400km of modern highway, and extensive seaports along its coast.

However, the Mexican economy is highly exposed to the US economy, its largest trading partner. Near-term, trade tension can cause uncertainties in the Mexican economy. In addition, Mexico’s new president has been a proponent of constitutional reforms, which introduces uncertainties for the country.

Brazil is a growing, vibrant, commodities rich country, with a vast population (~216mn) that is well off from an economic perspective. Brazil is a major exporter including soybean, oil, iron ore, and proteins. The longer-term fundamentals of the Brazilian economy are robust.

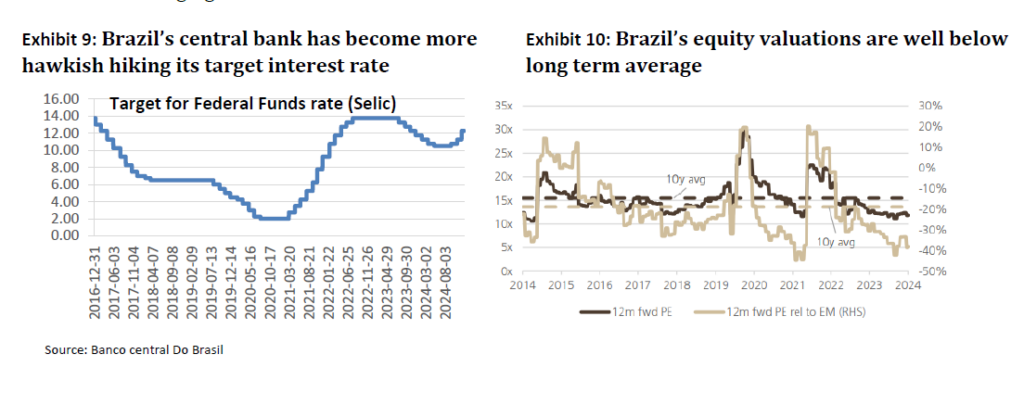

• In recent months, Brazil’s central bank has turned more hawkish, raising its target interest rate (Selic rate) from 10.5% to 12.25% and targeting two more rate hikes of one percent each in the first quarter of 2025.

• The central bank is hiking to dampen persistent inflationary pressures, while supporting the currency.

• The rate hikes reflect a balancing act as policymakers navigate the complexities of a volatile global environment and domestic fiscal concerns. Equity valuations are now at depressed levels.

• The short term outlook in Brazil is less prospective relative to other emerging markets given the counter-cycle stance of the central bank in the near-term, but we believe long-term opportunities are emerging.

India: Attractive long-term fundamentals, but economic slowdown will impact equity performance

The economy in India has been going though economic reforms over the last decade. However, it took the banking system just as long to recover from the last capital expenditure boom bust cycle. India has a vast population with over 1.4bn people, but income levels are low. It is a rising power, which adroitly manages relationships between USA and China.

• Recently, there are clear signs that the economy is slowing down after several years of strength post-COVID. We are seeing weak loan growth amongst banks, a worsening credit cycle in the credit card and micro-finance sectors. The sudden slowdown in economic activity caught many companies unaware. Almost 50% of companies in the market missed their quarterly earnings recently. On average, they were expected to grow earnings 9% from a year prior, but many companies reported barely flat earnings. Furthermore, many sectors were caught up, including autos, consumer stables, power generators.

• Apparently, Indian consumers have exhausted their excess savings accumulated during COVID. Similar to other economies, urban consumers in India are squeezed by higher cost of living, such as rental and slowing wage growth. This round of consumption slow down coincides with tighter spending discipline by the government, as well as higher interest rate. As inflation is currently running “hot”, chances of rate cuts have diminished.

• Despite macro-economic uncertainty, valuation of the market remains expensive. With growth slowing down, the sky-high valuation will likely not be sustainable.

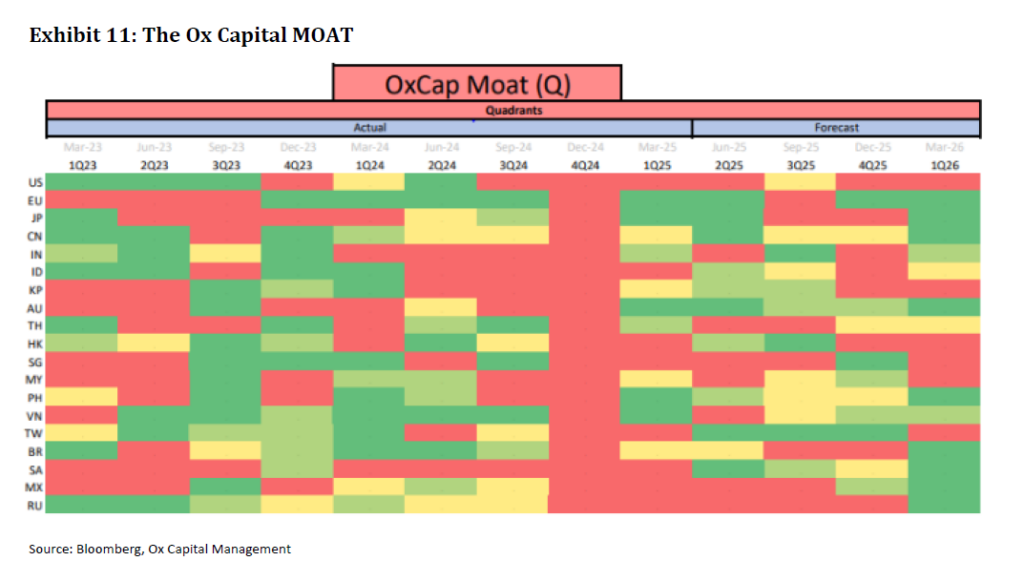

The MOAT (Macro Overlay Aggregate Tracker):

Our risk management framework at Ox Capital relies on both quantitative and fundamental, bottom-up analysis along with our experience to deliver actionable, alpha generating ideas. Our propriety quantitative model is pointing to a promising environment for EM growth in 2025 as inflation in many economies is stable to declining. We note:

• Asia’s outlook remains positive through the year.

• The Chinese economy is putting in a bottom and outlook is improving throughout 2025.

• Indonesia’s and Vietnam’s outlook remains positive.

• Taiwan’s growth profile continues to be strong and improving.

• LATAM remains challenging near-term.

• Both Brazil and Mexico are less prospective in 2025

• In contrast, the outlook looks challenged for US through the year.

In summary, we believe we are at an inflection point for EMs and current valuations are providing an attractive entry point. Many EM countries have strong underlying economic fundamentals. Inflation is trending lower in many EMs allowing central banks to cut rates while a slower global growth outlook is set to benefit emerging economies with endogenous growth drivers.

The recent USD strength and inflationary impulse in the US has made US products and wages expensive compared to the rest of the world. The decreasing competitiveness argues for a weaker USD, which can be triggered if signs of slowing US economic growth emerges. We reiterate the persistent large federal government debt and the uncertainties in implementation of new US government policies are likely to temper expectations of continue USD strength, especially given its significant appreciation to date.

The leading quality companies within the Ox Capital portfolio are taking market share domestically and globally. Valuations remain highly attractive. In our view, their potential is under appreciated.

Now is the time to invest and take advantage of attractive valuations for quality franchises with profitable long-term sustainable growth across Emerging Markets.

At Ox Capital, we are focused on quality companies with long term growth which are available at inexpensive valuations across emerging markets. Current valuations are providing lots of interesting opportunities. Let us know if you would like to understand specifically where we are finding the opportunities!

Important Information: This material has been prepared by Ox Capital Management Pty Ltd (Ox Cap) (ABN 60 648 887 914) Ox Cap is the holder of an Australian financial services license AFSL 533828 and is regulated under the laws of Australia. This document does not relate to any financial or investment product or service and does not constitute or form part of any offer to sell, or any solicitation of any offer to subscribe or interests and the information provided is intended to be general in nature only. This should not form the basis of, or be relied upon for the purpose of, any investment decision. This document is not available to retail investors as defined under local laws. This document has been prepared without taking into account any person’s objectives, financial situation or needs. Any person receiving the information in this document should consider the appropriateness of the information, in light of their own objectives, financial situation or needs before acting. This document is provided to you on the basis that it should not be relied upon for any purpose other than information and discussion. The document has not been independently verified. No reliance may be placed for any purpose on the document or its accuracy, fairness, correctness, or completeness. Neither Ox Cap nor any of its related bodies corporates, associates and employees shall have any liability whatsoever (in negligence or otherwise) for any loss howsoever arising from any use of the document or otherwise in connection with the presentation.